How Does Blockchain Work?

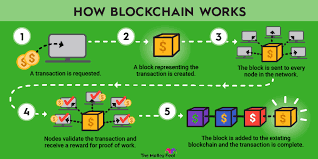

Blockchain works by storing data in blocks that are linked together chronologically. Each block is encrypted and connected using cryptographic hashes.

It's decentralized—meaning no single authority controls the network. Instead, consensus mechanisms like Proof of Work or Proof of Stake validate transactions.

Once verified, blocks become a permanent, tamper-proof part of the chain.